However, I’ve been in the business for 10 years, and have benefited from a growing economy, cheap debt, and compressing cap rates. I have yet to experience a down market as a working professional. At some point, this bull market will end, and we’ll experience a recession.

When that inevitably happens, what will the impact be on the Class B apartment sector? That’s something I think about often as we continue to acquire value-add multifamily apartments.

Before delving into the various scenarios that lead to a recession, I wanted to look at the multifamily sector from a general investment perspective. Multifamily is uniquely attractive due to the following asset-level attributes:

- Multifamily properties have averaged approximately 94% occupancy over the past 15 years and have never averaged below 91%.

- Apartments’ average return over a 30-year period is the best of the primary property sectors, averaging 12%.

- Apartments have the most efficient cash flow and typically convert 83% of NOI into cash flow.

- Apartments have the lowest re-tenanting costs and typically have the lowest cost of debt.

- Apartment rents adjust daily, making them more reflective of changing market conditions.

- Apartments have historically experienced much lower volatility with respect to income and valuations relative to other property types.

These attributes make multifamily attractive relative to other real estate asset classes. However, it’s the drivers behind these statistics which need to be fully understood to begin to think about how the asset class may react during a downturn. Over the past 10 years, multifamily demand has been driven by the confluence of population, income, and wage growth, combined with a lack of new supply and a cyclical shift toward renting (couples getting married later or not at all, tighter lending standards, increasing income inequality etc.). Class B/C multifamily assets have been the primary beneficiaries of the increased demand. Here are some stats from a recent CBRE report.

- Q1 Vacancy – the lower classes had fewer vacant units relative to the totals of each class.

- Tightest vacancy rates in Class C (4.5%)

- Class B vacancy was 5.0%

- Class A was 5.6%

- Q1 Growth – similarly, rental growth was higher in the lower-class categories.

- Class C’s year-over-year rent growth was averaging 3.0%

- Class B 1.6%

- Class A’s 0.7%

- Older product has been outperforming newer product. Garden product has been outperforming high-rise.

- CBRE EA’s Q2 statistics revealed 4.8% vacancy rates for multifamily units built in the 1960s, 1970s, and 1980s

- As of Q2 year-over-year rent growth for garden properties averaged 3.3% vs. 1.2% for high-rise communities

The class B/C multifamily sector has enjoyed a prolonged period of growth, with no signs of slowing. However, how will these assets perform during a downturn?

Let’s explore further by looking at the drivers of real estate cycles.

Real Estate Cycles

Supply/Demand

Real estate cycles are prolonged periods of supply/demand imbalance. Building a new multifamily property can take 24-48 months, and although the market was at equilibrium (or demand outweighed supply) when you embarked on the project, that may not be the case when you’re leasing up. In a weaker market, you’re forced to lower rents and offer concessions. This won’t last forever, but the market adjustment can take a long time given the construction timeframe (more units may be under construction even though the demand weakened). From here, it takes demand growth to close the supply-demand gap.

On the demand side, the population grows at about 0.75% per year and the economy adds about 1.7 million jobs per year on average (on a national level). That may vary from market to market, but over time supply with slow and the growing demand will absorb the units on the market, albeit at discounted rents.

When there’s an oversupply of multifamily real estate, the newly constructed communities leasing up in a soft market will offer concessions and lower rents. This may have a trickledown effect, forcing class B/C communities to lower rents. However, as the low-cost value option, class B/C communities have some pricing power. There just is no lower priced, quality housing for median-income earning residents. Ultimately, rents may come down, but I think the rent gap between class A and B will narrow.

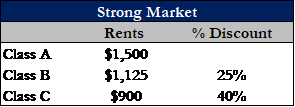

Here’s a simple example:

In a strong market, class B rents may be a 25% discount to class A and class C rents may be a 40% discount to class A. If the market becomes over-supplied and class A properties discount their rents by 10%, class B/C properties will be forced to discount their rents as well. However, since class B/C is largely buffered from new supply, their rents will not drop nearly as much, and although the gap between class B/C and class A rents will narrow, there is still a large enough gap where cost-constrained renters will choose the lower cost value option.

Capital Flows

In addition to supply/demand imbalances, real estate cycles can be driven by the flows of capital. If debt and equity is cheap and plentiful, real estate owners will overpay and overleverage. This was the driver behind the 2008-2009 financial crisis. Cheap debt, limited credit checks, and greed went too far, and the Financial Crisis was triggered by defaults on subprime residential mortgages. When the RMBS market imploded, owners/investors lost their homes and the credit markets lost credibility.

When capital retreats from the real estate market, it’s driven by a downturn in the economy. In this scenario, many former homeowners were forced into rentals as they must live somewhere, and the beneficiary was the low-cost, high-value class B/C apartment communities. In these times, renters ignore the allure of highly-amenitized Class A communities, as they’re just happy to live somewhere and even a small price differential won’t convince them to overspend on housing.

I’d argue that in a down economy, demand for lower-end, but quality, apartment communities experience increased demand and thus may even be able to increase rents during that period. See the chart below. Apartment rental growth may slow at times but generally outpaces inflation across cycles.

All that said, we’re in the midst of the 2nd longest economic expansion in history and due for some sort of reset. While multifamily may react a bit differently to changes in rates/capital flows, stepping back to the big picture, there are just so many offsetting factors that I think would tend to keep things in a relative equilibrium. I anticipate modest ups and modest downs, until a major event causes disruption to the capital markets, causing a shortage of debt, making equity more expensive, and driving prices down in a big way (for a short period of time, hopefully, followed by a sharp recovery).

However, as an operator, I’m comfortable owning high-quality Class B apartment communities in submarkets experiencing strong population and employment growth that also have high-barriers to entry. I believe these assets will perform best over the long-term and by maintaining conservative leverage and sufficient cash reserves, we can weather any sort of downturn in the economy.

That said, I was having a conversation with a well-respected acquisition professional for a multifamily owner-operator who’s been in the business for 30+ years. He’s lived through several cycles and is well-respected in the industry. He has one rule. “Never buy class C”. So what do I know?

What do you think? Have you seen any data which suggests class B/C underperform other asset classes during a downturn?