The demand for multifamily remains strong, but the drivers of demand are often different than what most people think. Tell me if you’ve heard these two narratives:

- Millennials are moving more often so they prefer the flexibility of renting.

- Millennials have a shifting preference toward renting over buying.

I’ve heard these from many smart real estate professionals who typically use anecdotal evidence to support their claim. While Millennials are staying in the renter pool longer, it’s generally not because of the reasons noted above.

Let’s start with the first myth that increased mobility has led to stronger demand for rentals. This claim is easy to debunk empirically. The Census Bureau records annual migration statistics. For the first time ever since the Census Bureau began tracking back in 1947, fewer than 10% of Americans changed residences in 2018/19.

This data captures both local moves (within counties) and longer-distance moves (across counties). For the sake of this argument, let’s focus on the long-distance moves.

Cross-county movement has hovered between 3.5-3.7% since 2007. Prior to this, cross-county mobility levels were 4% or higher, including rates in the 5-6% range in the 1990s.

Drilling down into the 18-34 cohort, historically the most mobile age, you can see that young people aren’t moving as much as they used to. The chart below shows the rates of mobility by age in 2005-06 and 2018-19. Young adults, the group with highest rates in both years, also showed the largest decline in mobility rates. For example, among young people aged 20-24, only 20% made a move in the most recent year, down from 29% in 2005-06.

Millennials are stuck in place for the same reason they’re stuck in the renter pool; housing costs, underemployment, and student debt which lead to delaying marriage, having kids, and ultimately buying a home.

The rise of remote work also plays a factor. As companies embrace remote work and technology is developed to support it, people have access to wider pool of jobs without having to relocate.

The census data show that the annual migration rates of renter households have declined precipitously over time (from 30.2% in 2005-06 to 19.7% in 2018-19). The data is clear, young people aren’t moving as often as they used to. Not surprisingly, apartment retention rates are at an all-time high.

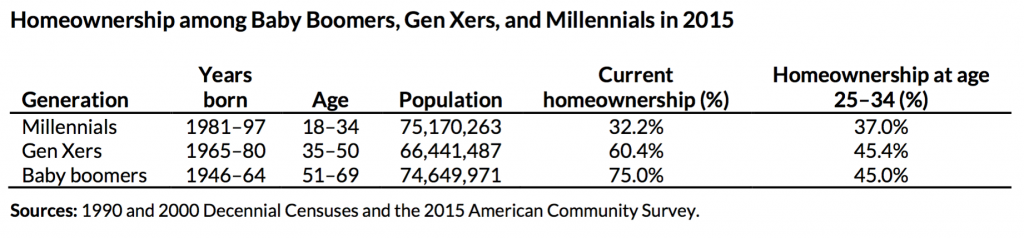

This is a good segue into the next myth; Millennials have a stronger preference to rent instead of buy. This is a bit trickier to disprove empirically, but there are several data points that show a continued preference toward buying over renting. To lay out this argument, I’m going to dig into the factors which typically impact homeownership; marriage and kids, debt, and demographics.

Millennials are delaying marriage and having kids. Why? This is in part driven by the influx of women in the workplace and individuals desire to advance their career prior to settling down. Additionally, young people want a strong foundation so they can get marriage right. However, many people also cite student debt and high housing costs as reasons to postpone marriage and kids. “Marriage used to be the first step into adulthood. Now it is often the last.” Being married increases the probability of owning a home by 18%.

Student-loan debt is much higher. A study by Urban.org found that for every 1% increase in student loan debt, the likelihood of owning a home decreased by 0.15%. Student loan debt has skyrocketed in recent years, driving down the likelihood those individuals purchase a home. It takes student debt-burdened college grads about 12 years to save 20 percent for a down payment.

Changing racial diversity also plays a role. White households have a higher ownership rate than other racial groups. Millennials increasing diversity has led to lower homeownership rates. Between 1990 and 2015, the share of white households dropped by 16% from 76% to 60%.

The factors above explain why rental demand has remained strong and the homeownership rate has dipped. However, as soon as young people get married and have kids or can afford to buy a home, they do so. Married couples with 2 or more kids have a homeownership rate of 80%.

Now let’s look at the average down payment. In 2019, the average down payment was just 5.3% and 46% of all homebuyers put down less than 5%. While it could be argued that home purchasers prefer to put down as little as possible, I think this data shows that most people who can get approved for a mortgage opt to buy a home.

Suffice it to say, attitudes of Millennials toward homeownership have not changed much from prior generations, but other factors impacting their ability to buy homes have.

Sources

- https://www.npr.org/2019/11/22/781930048/low-mobility-rate-has-consequences-for-families-and-the-economy?mod=djemDailyShot&mod=djemDailyShot

- https://www.urban.org/urban-wire/state-millennial-homeownership

- https://www.brookings.edu/blog/the-avenue/2019/11/22/for-the-first-time-on-record-fewer-than-10-of-americans-moved-in-a-year/